Switching your checking account to an app feels risky when nobody at the company can hand you a printed statement or sit across a desk.

The Albert Cash Account pitches itself as a full checking replacement. No branches, no minimum balances, no monthly fees. Everything runs through a phone.

But Albert itself is not a bank. That single detail reshapes how the entire account works, and almost no comparison article treats it seriously.

Albert Is Not a Bank: So Where Does the Money Go?

The first thing to understand about the Albert Cash Account is the company behind it. Albert is a fintech app. It is not a chartered bank.

Deposits go to a partner institution that holds FDIC insurance up to $250,000. Albert handles the interface, the notifications, the budgeting tools. The partner bank holds the money.

This matters when something goes wrong. A disputed charge, a frozen account, a missing deposit: these situations involve two separate entities instead of one.

The app team and the bank team may not move at the same speed or share the same support queue.

Traditional banks keep everything under one roof, so a single phone call can often resolve the issue. The Albert structure adds a layer between the user and the institution holding the funds.

How FDIC Insurance Works Through Albert’s Partner Bank

The FDIC coverage is real. Funds in the Albert Cash Account are insured up to $250,000 per depositor, same as a traditional checking account at Chase or Wells Fargo.

The difference is that the app shows Albert’s name while the FDIC paperwork lists the partner bank’s name.

For someone opening their first digital-only account, this can feel confusing. The coverage works. But the path to filing an FDIC claim, if it ever came to that, runs through the partner bank rather than Albert’s support team.

Daily Banking on the Albert Cash Account

The day-to-day experience runs through a single app. Account setup, direct deposit enrollment, bill payments, and transfers all happen on screen. No paper forms and no teller windows.

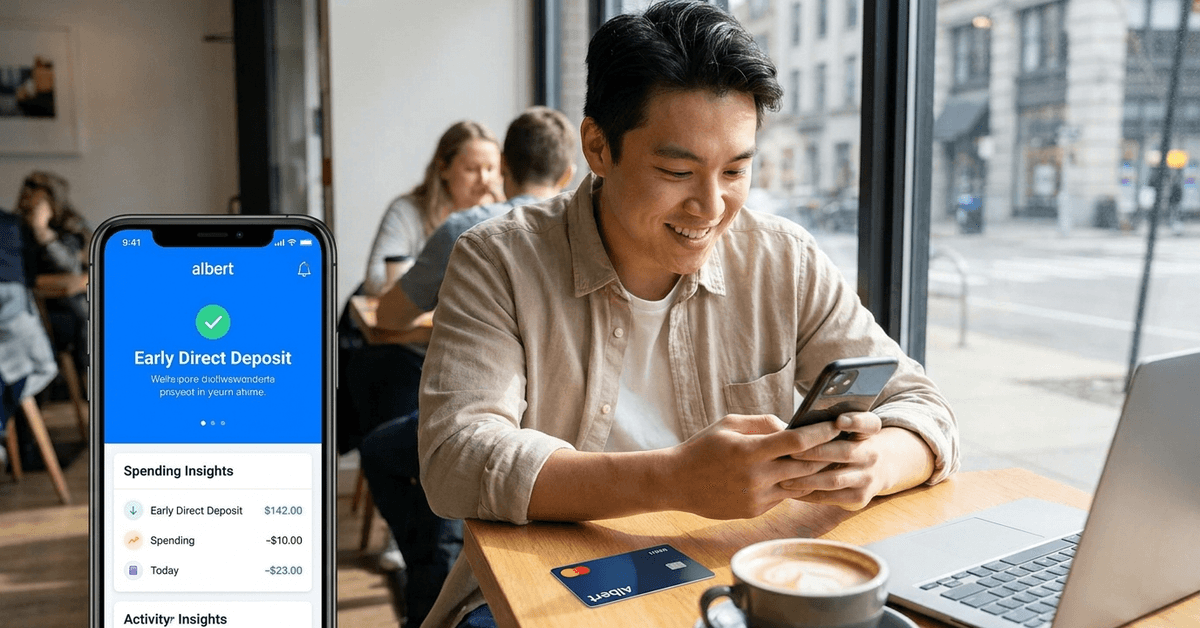

Early Direct Deposit: Up to 2 Days Faster

Albert offers early access to paychecks, potentially up to two days ahead of the standard pay date. This depends entirely on the employer’s payroll system. If the employer sends the deposit early enough, Albert releases the funds sooner.

This is a selling point across nearly every digital checking app in 2026. Chime, Current, and Varo all advertise similar timelines.

The speed comes from the payroll provider, not from the app itself. So comparing early deposit claims across these four apps is a bit like comparing speed limits on the same highway.

I think the emphasis on “get paid 2 days early” across Albert, Chime, and Varo is misleading because the timing depends on payroll processors, not the app.

A reader comparing these four platforms on early deposit speed alone would be making a decision based on a feature none of them fully control.

No Minimum Balance and No Monthly Fee

Albert does not require a minimum balance. There is no monthly maintenance fee. The account stays open and active regardless of how much sits in it.

This is a strong fit for anyone whose income fluctuates: gig workers and freelancers between steady paychecks. A traditional checking account at a large bank often charges $10 to $15 per month if the balance drops below a set threshold.

Debit Card and Mobile Payments

The account comes with a debit card that works at ATMs and retail locations. It also connects to mobile payment platforms for tap-to-pay transactions.

ATM access depends on the network. Pulling cash from an out-of-network ATM may come with fees from both the ATM operator and Albert’s partner bank.

Check the current fee schedule on Albert’s official app page before relying on ATM withdrawals as a regular habit.

Where the Albert Cash Account Falls Short

No app-only checking account covers every banking need. Albert has specific blind spots that matter more for certain users than the glossy feature list suggests.

Cash Deposits and the Retailer Workaround

Depositing physical cash into an Albert Cash Account requires visiting a partner retailer. That visit may come with a third-party fee. For anyone who regularly receives cash payments, tips, or side income in paper bills, this is a real friction point.

Traditional banks and credit unions accept cash deposits at no cost. Digital-only accounts almost universally struggle here, and Albert is no exception. If a noticeable chunk of income arrives in cash, this limitation shapes the entire banking experience.

No Loans, No Mortgages, No Investment Tools

Albert is built for daily money movement. The account handles spending, saving, and transferring. It does not offer mortgage products, personal loans, or investment accounts.

Anyone who wants all their finances in one place will still need a second institution. That might be fine if the Albert Cash Account handles the daily flow. But it does mean managing two logins, two customer service teams, and two sets of statements.

The Cash Advance Feature and Its Limits

Albert offers small emergency cash advances to qualifying accounts. The amounts are typically modest. And qualifying depends on account activity, direct deposit history, and other internal criteria that shift over time.

I would not recommend choosing Albert over Chime or Varo based on the cash advance feature, because the advance amounts are too small to cover a real emergency and the eligibility requirements change based on activity the user cannot always predict.

Chime’s SpotMe feature, for comparison, goes up to $200 for qualifying users with a clearer set of criteria.

Albert Cash Account vs Chime vs Current vs Varo

A side-by-side comparison helps sort out where each app fits. All four target mobile-first users who want to skip traditional banking, but the differences between them are worth examining closely.

| Feature | Albert | Chime | Current | Varo |

|---|---|---|---|---|

| Monthly Fee | $0 | $0 | $0 ($4.99 premium tier) | $0 |

| Early Direct Deposit | Up to 2 days | Up to 2 days | Up to 2 days | Up to 2 days |

| Cash Deposits | Partner retailer (fees may apply) | Partner retailer (fees may apply) | Partner retailer | Partner retailer |

| Savings Interest | Limited | Competitive APY | Limited | Competitive APY |

| Cash Advance | Small amounts, qualifying users | SpotMe up to $200 | None standard | Varo Advance |

| FDIC Structure | Through partner bank | Through partner bank | Through partner bank | Direct (Varo Bank, N.A.) |

Varo is the only one on this list that is an actual chartered bank.

That distinction means FDIC insurance flows directly through Varo rather than through a partner arrangement. For someone who cares about that structural difference, Varo has a clear edge.

Picking Between These Four

The savings interest rate is where Chime and Varo pull ahead of Albert. If the goal is to park some money and earn on it, Albert’s limited rate falls behind.

Albert’s strength is its budgeting and automated savings tools, which appeal to users who want the app to manage spending behavior rather than just hold funds.

Setting Up an Albert Cash Account

The signup process runs through the app and typically finishes in minutes. These are the requirements:

- A valid U.S. government-issued photo ID

- A Social Security Number

- Age 18 or older

- The Albert app downloaded from the App Store or Google Play

- U.S. residency (terms and features may vary by state)

Some applications receive instant approval. Others get flagged for additional identity verification, which can add a few days. Discrepancies between the ID and the information entered on the form are the most common cause of delays.

Fees to Watch After Opening

Albert promotes a low-fee structure, but a few charges can still appear:

- Out-of-network ATM withdrawal fees from the ATM operator or partner bank

- Third-party fees at cash deposit retail locations

- Fees tied to expedited cash advances for eligible users

The Consumer Financial Protection Bureau publishes guides on evaluating digital bank fee structures. Checking that resource alongside Albert’s account agreement gives a clearer picture of total costs.

Data Privacy and Marketing

Albert states it shares data for operational needs or as required by law. Account activity may inform marketing within the app. A preference center inside the app lets users adjust how much promotional content they see.

Anyone wary of data sharing should review the privacy policy during signup. Doing it after the account is open is too late to make an informed choice.

Questions People Ask About the Albert Cash Account

A few questions come up repeatedly when people research Albert as a digital checking alternative.

Q: Is the Albert Cash Account free to open and maintain?

The account has no monthly fee and no minimum balance requirement. Out-of-network ATM fees and cash deposit charges at partner retailers still apply, so “free” depends on how the account is used day-to-day.

Q: Can physical cash be deposited into the Albert Cash Account?

Cash deposits go through partner retailers, which may charge a separate fee per transaction. This is one of the biggest drawbacks for anyone who handles physical cash regularly, especially gig workers or tipped employees.

Q: Is Albert FDIC insured in 2026?

Funds are FDIC insured up to $250,000 through Albert’s partner bank. Albert itself is not a chartered bank, so the insurance runs through the institution holding the deposits rather than through Albert directly.

Q: Does Albert offer investment accounts or loans?

Albert has automated savings features and budgeting tools but does not offer investment accounts, mortgage products, or personal loans. A separate institution would be needed for those services, which adds another account to manage.

Q: How does Albert’s early direct deposit compare to Chime?

Both advertise up to two days early, but the actual timing depends on when the employer’s payroll processor releases the funds. Neither app controls that timeline, so the feature performs nearly identically across both platforms.

Conclusion

The Albert Cash Account fits a specific user well: someone who wants a simple, phone-based checking account without legacy bank fees. Cash-heavy users and anyone who needs loans or investment tools will run into limitations fast.

The “not a bank” structure behind Albert deserves more scrutiny than it typically gets in feature comparisons. Spending ten minutes reading the partner bank disclosures before signing up is time well used.