Best Credit Cards for Your Profile matters more in 2026 than another generic “top cards” roundup. AI models and fintech tools now score cards against real spending patterns, fee tolerance, and approval odds, then surface the best-fit option for the way life actually runs.

That shift is the reason AI credit card recommendations keep showing up in personal finance apps, browser extensions, and bank dashboards.

Done well, the result feels less like shopping and more like reducing waste: fewer unused perks, fewer surprise fees, and rewards that show up where spending already happens.

Why Profile-Based Picks Beat Top-10 Lists

Card marketing is built around averages. Real budgets rarely are. A frequent traveler who books flights and hotels gets value from lounge access and travel credits that a homebody never touches.

A person rebuilding credit needs a clean, predictable path to on-time payments, not a complex points system. Profile-led selection also helps prevent a common mistake: choosing a card for the headline rewards rate, then losing money to annual fees, interest, or missed category rules.

AI-driven tools try to solve that mismatch by focusing on net value. Net value means rewards and credits earned minus fees paid, plus a reality check on whether the card’s rules fit everyday behavior.

What AI Looks At When Matching Cards

Personalized models usually start simple, then get more specific as more data becomes available. A platform may ask questions, connect transaction data, or both. A strong personalized credit card match depends on accurate inputs and honest expectations about spending.

Common data points include:

- Spending breakdown (groceries, dining, travel, fuel, bills, business tools)

- Payment behavior and credit utilization (how much of the limit gets used)

- Credit score band and credit history depth

- Fee tolerance (preference for $0 annual fee vs premium perks)

- Primary goal (cash back, travel points, credit building, business expenses)

Some systems also consider alternative signals. Lenders and fintech platforms have discussed using broader data to refine risk decisions, though the availability and legality of specific data sources vary widely by country.

Best Cards By Profile

Different profiles call for different “best” answers. The picks below reflect widely discussed, AI-forward recommendations seen across major personal finance ecosystems as of early 2026, then grounded in issuer-published benefit structures and terms that can be verified.

Best For High-Spend and Frequent Travel

Capital One Venture X Rewards Credit Card often ranks as a top travel rewards credit card because the perks are straightforward to value. Capital One markets lounge access through Capital One Lounges plus Priority Pass access (after enrollment), and a $300 annual travel credit that applies to bookings made through Capital One Travel.

Chase Sapphire Reserve® tends to show up as an alternative when maximum travel flexibility and redemption ecosystems matter.

American Express® Gold Card also appears for heavy dining and food spenders, though it plays a different game: strong earning categories paired with a higher-fee lifestyle bundle that only works if credits are actually used.

Best For Everyday Cashback and Low Maintenance

Citi Double Cash® Card is the classic flat-rate cash back card for people who want consistency. Citi advertises 2% cash back on purchases, structured as 1% when buying and 1% when paying, with no category activation and no annual fee.

That “set it and forget it” structure is why it keeps showing up in simplified recommendations.

Chase Freedom Unlimited® is a common alternative when someone wants a slightly more complex setup that boosts specific categories while still earning a baseline rate elsewhere.

Best For Food, Groceries, and Family Spending

Blue Cash Preferred® Card from American Express often wins for grocery and dining cash back when U.S. supermarket spending is meaningful.

American Express advertises 6% back at U.S. supermarkets on up to $6,000 per year in purchases, then 1%, and added earnings on select everyday categories. This card can outperform a flat-rate option for households that reliably hit groceries and related spending.

Annual fees and category definitions matter here. Warehouse clubs, superstores, and local equivalents may not code the way someone expects, so the “grocery” assumption needs a quick verification against the issuer’s category rules.

Best For Beginners and Credit Building

Beginners usually need a beginner credit-building card that is easy to manage and has few gotchas. Discover it® Student Cash Back is commonly recommended for students because Discover promotes an end-of-first-year cash back match, with no annual fee.

Capital One Platinum Secured is another common route, using a refundable security deposit to open a credit line. Capital One explains secured cards as deposit-backed accounts designed for building or rebuilding credit.

cred.ai is the more unusual option. The “Unicorn Card” is positioned as a credit card with automation designed to prevent overspending and manage balances to optimize credit utilization. It’s often discussed as a safety-rail product for people who want credit-building behavior to feel more automatic.

Best For Small Business Spending

Chase Ink Business Cash Card often appears as a top small business credit card because the reward categories match common operating costs. Chase promotes 5% cash back on office supplies and certain business services such as internet, cable, and phone, with no annual fee.

This works well for owners who have steady spend in those categories and want predictable cash back. Brex Card frequently shows up for venture-backed startups or newer companies that prefer not to rely on a founder’s personal guarantee.

Brex describes corporate card underwriting that focuses on the business rather than personal credit in many cases, though eligibility depends on the company’s profile and region.

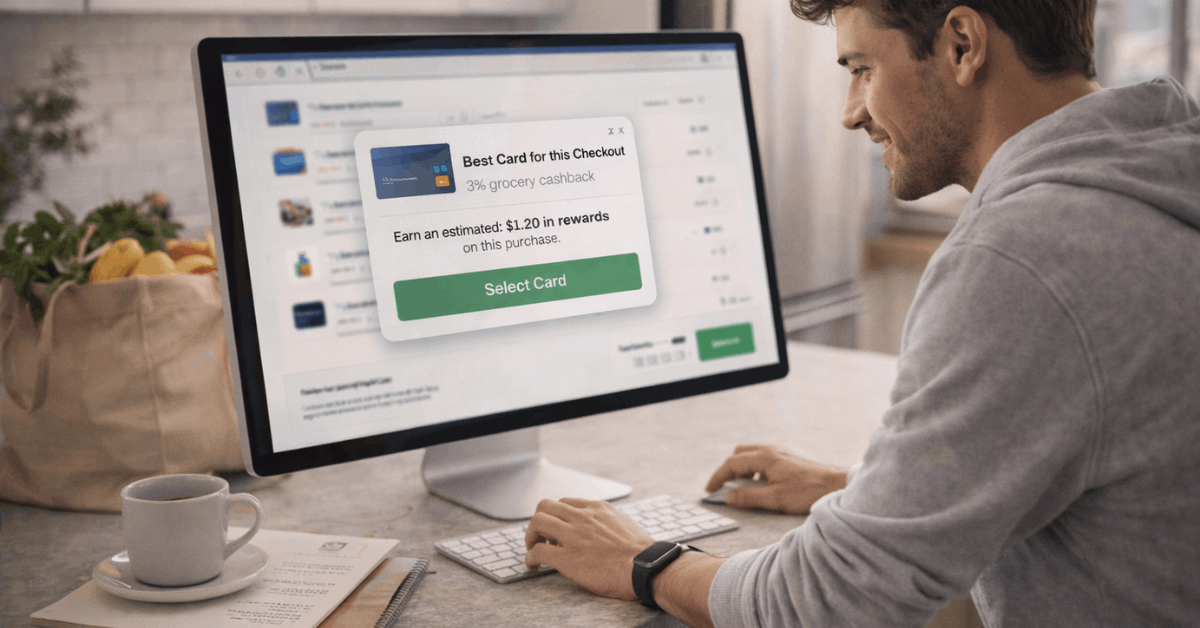

AI Tools That Help You Pick The Right Card

A credit card rewards optimizer typically sits in one of three places: a browser extension that helps at checkout, a fintech app that analyzes transactions, or a credit-focused platform that pairs recommendations with credit coaching. The best tool depends on the goal.

| Platform | Key Feature | Best For | Typical Cost |

| Kudos | Browser extension that recommends the best card per purchase | Maximizing rewards across multiple cards | Often marketed as free |

| GigaPoints | Spending analysis mapped to reward programs | Finding the best card for your spend | Often positioned as free tools |

| CheQ Wisor | AI-driven credit card insights inside a bill-pay ecosystem | Tracking usage, rewards, and guidance | App-based pricing varies |

| CreditCaptain | AI-guided credit improvement plus card suggestions | Credit-focused users aiming to qualify for better cards | Paid plans are marketed |

Kudos has been described publicly as a browser extension and app that helps select the best card for a given checkout, which fits people already holding multiple cards.

GigaPoints has positioned itself as a spending-driven recommendation platform that estimates reward value based on past spend. CheQ has publicly announced CheQ Wisor as an AI-powered credit card expert focused on spend insights and guidance.

CreditCaptain markets paid credit-improvement plans and describes AI-driven dispute and monitoring features, though pricing and claims should be checked carefully against the current terms.

How To Sanity-Check An AI Recommendation

AI can narrow choices fast, but a quick review prevents expensive mismatches.

- Start with approval reality. A premium travel card recommendation means nothing if credit history can’t support approval yet.

- Next, confirm net value: annual fee minus credits and realistic rewards earned.

A card that “wins” in an AI ranking can still lose if travel portals won’t be used, categories don’t match local merchants, or rewards get redeemed poorly.

Interest risk also deserves a blunt check. Paying in full each month keeps rewards meaningful. Carrying balances often wipes out rewards, even on high-earning cards.

Privacy, Bias, and Safety Checks

Transaction-linked tools require trust. Strong security basics still apply: multi-factor authentication, careful permissions, and a preference for platforms that explain data handling clearly.

Recommendation bias is also real. Affiliate-driven lists may push cards that pay the platform more, not cards that fit better. Cross-checking two tools plus issuer terms usually exposes weak recommendations quickly.

Human oversight matters most during life changes. Income shifts, moving countries, switching jobs, or starting a business can change the best fit overnight, even if spending stays similar.

Final Takeaway

Best Credit Cards for Your Profile is a moving target, and AI tools help track it without doing spreadsheet math every month. The smartest approach combines automated matching with basic self-audits: confirm eligibility, validate the real value of perks, and keep an eye on fees and interest.

Credit cards change terms, rewards rotate, and personal priorities shift, so a “best” card should feel like a fit right now, not a permanent identity.

Disclaimer

This site provides general information on credit cards and payment products, not financial, legal, or tax advice; always verify rates, fees, and terms with the issuing bank before applying.